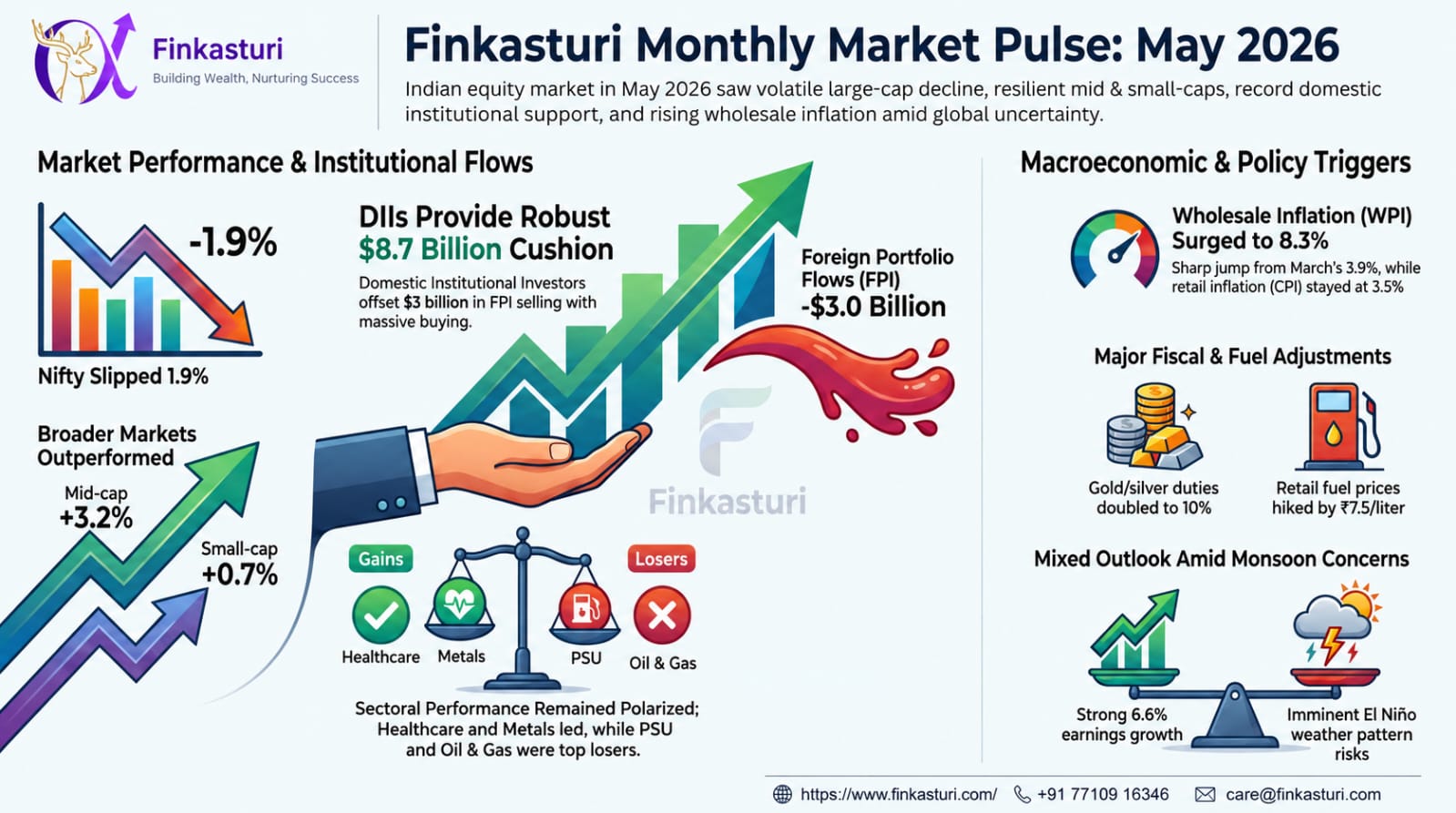

The Month That Was : September 2025

Indian equity markets ended September with modest gains, as the Nifty 50 Index rose by 0.8%. Broader markets outperformed slightly, with mid-cap and small-cap indices gaining 1.4% and 1.9%, respectively. Sectoral performance was mixed – metals, auto, and oil & gas indices rose by 9%, 6%, and 5%, while consumer durables, IT, and FMCG declined by 5%, 3%, and 2%, respectively.

Globally, South Korea, Mexico, and Hong Kong were the top gainers with returns of 7–8%.

Investor sentiment was supported by strong economic data, optimism around India-US trade talks, GST rate cuts, and the US Fed’s rate reduction. However, markets witnessed volatility after the US administration imposed a one-time fee on new H-1B visa petitions and announced a 100% tariff on branded drug imports. Key developments during the month were as follows - GST Council rationalizing rates with lower taxes on mass consumption goods and higher taxes on luxury/sin goods, Fitch upgrading India’s GDP growth outlook for FY26 to 6.9%, the US Fed cutting policy rates by 25 bps, and the Indian monsoon ending 8% above normal.

FIIs continued selling with a net outflow of USD 2 bn during the month in secondary markets while DIIs bought USD 7.4 bn.

Market Outlook:

Markets are expected to remain volatile in the near term until clarity emerges on trade deal between India and USA. Proactive steps by the Government to boost consumption and a downward trending interest rate cycle should aid in domestic economic growth. Pick up in consumption is already seen with festive season auto sales clocking around 20% growth on the back of GST rate reduction. Also, corporate earnings growth is expected to pick up in H2FY26 supporting the markets. We remain constructive on domestic and consumption oriented sectors such as banking, NBFCs, consumer discretionary, and consumer staples.

Happy Investing!

_1775458917.jpeg)