_1772702186.png)

The Month that was: February 2026

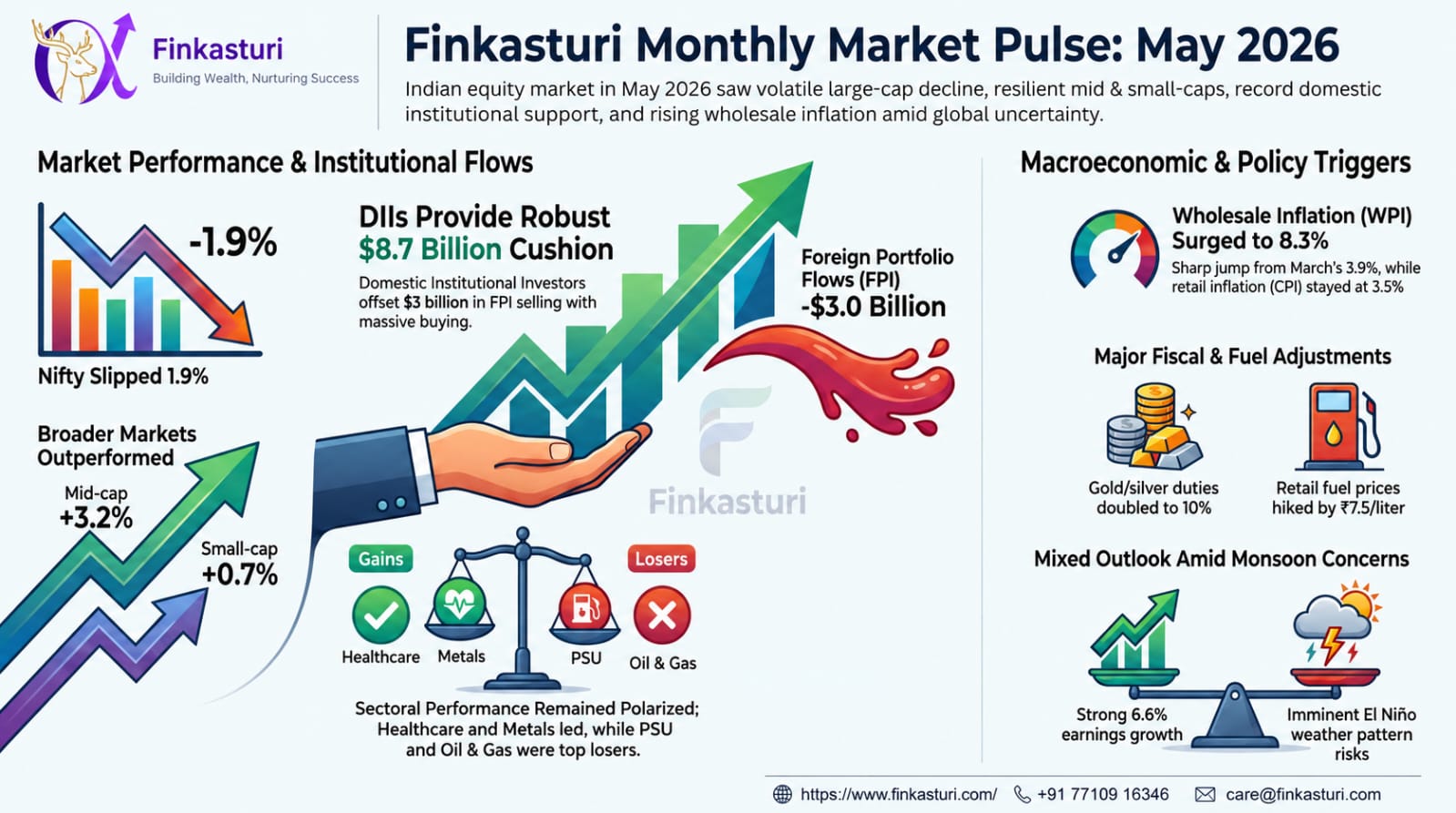

Indian equity markets recorded their third consecutive monthly decline, underperforming global peers. The Nifty index declined by 0.6%, while broader markets showed resilience, with the mid-cap and small-cap indices gaining 1.2% and 0.3%, respectively. Sectoral performance was largely positive, with Power, Consumer Durables, and Healthcare emerging as the top gainers, whereas the IT sector witnessed a sharp sell-off, declining 19% during the month. Globally, most markets ended positive, led by strong gains in South Korea, Thailand, and Taiwan.

Investor sentiment was dampened by rising geopolitical tensions between Iran and the US, as well as persistent concerns over AI-led disruption, which heavily impacted the IT sector following the unveiling of new automation tools by Anthropic. However, key positive developments included improving corporate earnings, with the Q3FY26 adjusted net income of Nifty50 index growing strongly. Additional tailwinds included the Indian rupee appreciating by 1.1%, alongside strong gains in gold and silver. On the macroeconomic front, the government targeted a fiscal deficit of 4.3% in the Union Budget for FY2027, while January CPI and WPI inflation stood at 2.75% and 1.8%, respectively. On the flows front, Foreign Portfolio Investors (FPIs) bought US$ 2 billion, while Domestic Institutional Investors (DIIs) bought US$ 4.2 billion in the secondary market during the month.

Market Outlook: Recent macro developments have been broadly positive for the Indian economy, highlighted by a balanced Union Budget FY2027, the successful conclusion of a key trade deal with the European Union alongside a landmark trade framework with the United States. Additionally, the US Supreme Court's ruling against reciprocal tariffs provides further relief for global trade dynamics. However, in the near term, Indian equity markets may navigate volatility stemming from ongoing geopolitical tensions in the Middle East and structural disruptions in the technology sector. Crude oil prices have gone up sharply due to war in the Middle East which doesn't augur well for India as we import the bulk of our crude oil consumption. A confluence of positive factors—such as robust corporate earnings growth, easing global trade tensions, stable domestic inflation, and steady institutional inflows from both FPIs and DIIs—provide a strong domestic foundation for Indian markets. These structural tailwinds position the broader market well for a resilient performance over the medium to long term.

Happy Investing!!

Stay Connected with FinKasturi For Linkedin: Click here!

For Instagram: Click here!

For any further details contact Finkasturi Nivesh on +91 7710916346 or care@finkasturi.com

Disclaimer: https://www.finkasturi.com/disclosures

_1775458917.jpeg)